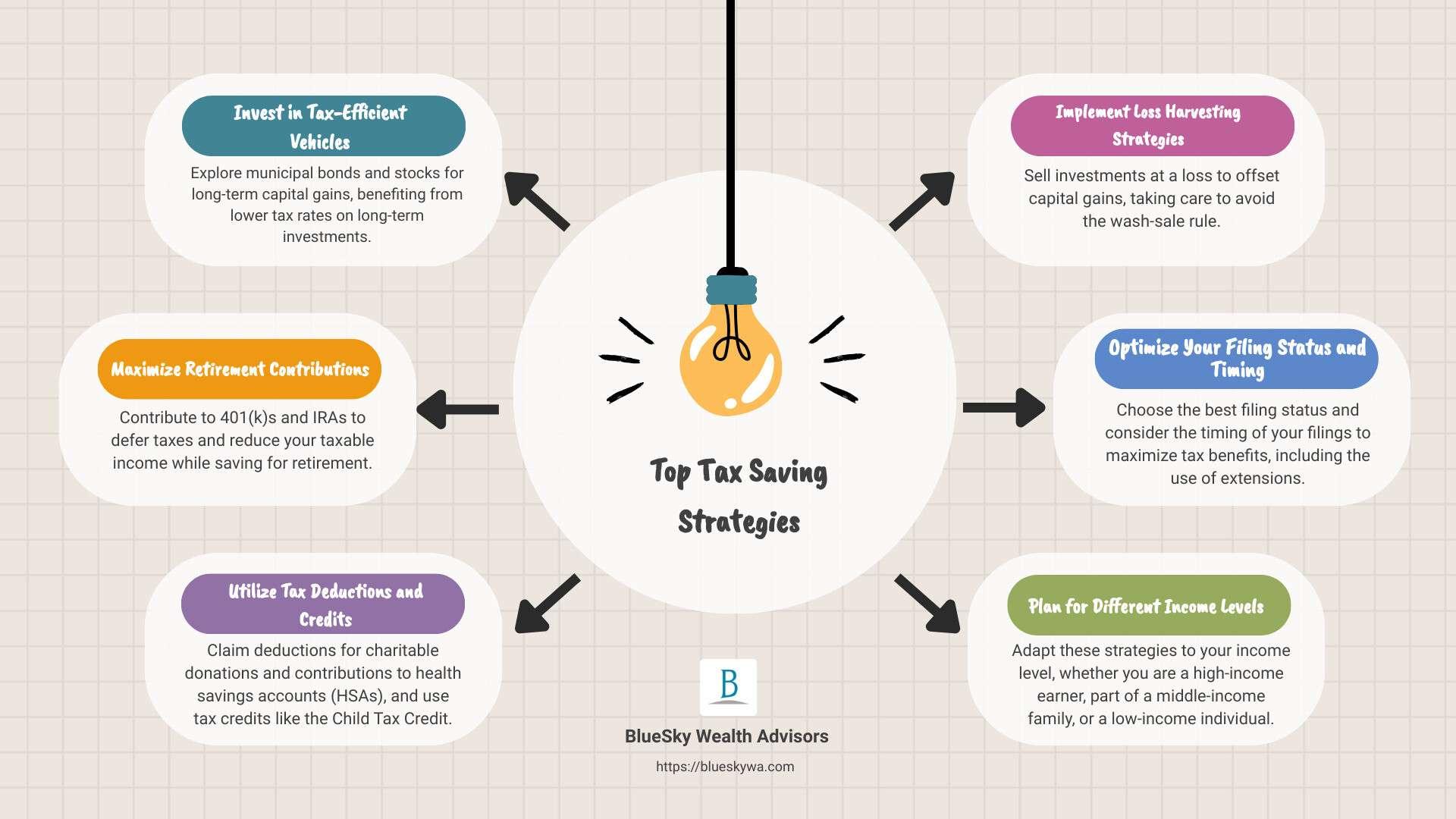

In the complex landscape of estate planning, navigating the intricacies of tax liabilities while preserving family wealth can seem like a daunting task. As estate taxes continue to pose a significant challenge for many individuals seeking to secure their financial legacy, the necessity of strategic planning becomes increasingly paramount. This article delves into the analytical aspects of estate tax reduction, offering a confident guide to implementing effective strategies that minimize tax burdens without compromising the financial well-being of future generations. By examining various tools and techniques, such as trusts, gifting, and charitable contributions, we aim to equip you with the knowledge to make informed decisions that safeguard your family’s assets and ensure a seamless transfer of wealth.

Understanding Estate Tax Implications and Exemptions

Estate taxes can significantly impact the wealth you intend to pass on to your heirs, but understanding the implications and exemptions can provide avenues to minimize these costs effectively. One of the key strategies involves making full use of the federal estate tax exemption, which, as of recent years, allows individuals to exclude a substantial amount from their taxable estate. Additionally, consider implementing a marital deduction, which permits the transfer of assets to a surviving spouse tax-free, thereby deferring the tax liability until the death of the second spouse.

Moreover, strategic gifting during your lifetime can be a powerful tool. By utilizing the annual gift tax exclusion, you can transfer assets incrementally, thus reducing the taxable estate. Consider setting up trusts, such as Irrevocable Life Insurance Trusts (ILITs) or Charitable Remainder Trusts (CRTs), to further shield your wealth from taxes while maintaining some level of control and benefit. These strategies not only help in minimizing estate taxes but also ensure that your family wealth is preserved and effectively managed across generations.

- Utilize lifetime gifting: Take advantage of the annual gift tax exclusion to transfer wealth without incurring taxes.

- Leverage trust structures: Establish trusts to protect assets and reduce taxable estate value.

- Maximize exemptions: Ensure full use of the federal estate tax exemption and marital deductions.

Strategic Gifting and Trust Planning for Wealth Preservation

Strategically planning gifts and trusts can be a powerful tool in reducing estate taxes while ensuring that family wealth is preserved for future generations. Gifting allows for the transfer of assets to family members during one’s lifetime, potentially lowering the taxable estate. By taking advantage of annual gift tax exclusions and lifetime exemptions, individuals can systematically reduce the size of their estate. Consider these effective gifting strategies:

- Utilize the annual gift tax exclusion to transfer assets tax-free.

- Leverage lifetime exemptions for larger transfers without incurring taxes.

- Establish Irrevocable Trusts to remove assets from your taxable estate, while still controlling the distribution to beneficiaries.

Trust planning offers another layer of protection and tax efficiency. By setting up specific types of trusts, such as Grantor Retained Annuity Trusts (GRATs) or Qualified Personal Residence Trusts (QPRTs), you can shift future appreciation out of your estate, minimizing estate taxes. Trusts not only provide a mechanism for asset protection but also ensure that your financial legacy is managed according to your wishes. The strategic combination of gifting and trust planning creates a robust framework for maintaining family wealth while navigating the complexities of estate taxation.

Leveraging Charitable Contributions for Tax Efficiency

When strategizing to minimize estate taxes, utilizing charitable contributions can be a highly effective approach. By integrating philanthropy into your estate planning, you not only contribute to meaningful causes but also benefit from tax deductions that can significantly reduce the taxable value of your estate. Here are some methods to consider:

- Charitable Remainder Trusts (CRTs): These trusts allow you to donate assets while retaining income for a specified period. After the term, the remaining assets go to the charity, providing you with an immediate tax deduction.

- Donor-Advised Funds (DAFs): Contribute to these funds to receive an immediate tax deduction, while having the flexibility to recommend grants to charities over time, aligning with your philanthropic goals.

- Qualified Charitable Distributions (QCDs): If you’re over 70½, consider directing required minimum distributions from your IRA to a qualified charity, thereby excluding the amount from taxable income.

Incorporating these strategies not only aligns with your charitable intentions but also safeguards your family’s wealth by efficiently reducing estate tax liabilities. By understanding and leveraging these options, you can achieve a balance between generosity and financial prudence.

Utilizing Life Insurance to Offset Estate Tax Liabilities

One strategic approach to alleviating the burden of estate taxes is through the judicious use of life insurance. This financial tool can serve as a powerful buffer, safeguarding your heirs from the potentially crippling tax liabilities that might otherwise erode the wealth you’ve painstakingly accumulated. By establishing an irrevocable life insurance trust (ILIT), you can ensure that the policy’s death benefit is excluded from your estate, thus providing liquidity to cover estate taxes without diminishing the core assets meant for your beneficiaries.

- Preserve Family Wealth: The death benefit from a life insurance policy can be used to pay estate taxes, ensuring that other assets, such as real estate or investments, do not need to be liquidated.

- Control Distribution: With an ILIT, you have the flexibility to dictate the terms under which the proceeds are distributed, allowing you to maintain control even beyond your lifetime.

- Mitigate Tax Impact: By keeping the insurance proceeds out of the taxable estate, you effectively reduce the overall tax liability, preserving more wealth for future generations.

Implementing life insurance as part of your estate planning strategy requires careful consideration and expert guidance. However, when executed properly, it can be a cornerstone tactic in ensuring your family’s financial security while minimizing tax implications.

{kind=link}